Al-Haq publishes our response to the request for submissions by the UN special rapporteur on the situation of human rights in the Palestinian territories occupied since 1967 calling for input on the private sector’s commission of international crimes connected to Israel’s unlawful occupation, racial segregation, and apartheid regime. The following is a summary of Al-Haq’s submission on the illegal activities of 501(c)(3) nonprofit organizations which directly enable and facilitate the spread of illegal settlement activity throughout occupied Palestine in furtherance of Zionist settler-colonialism.

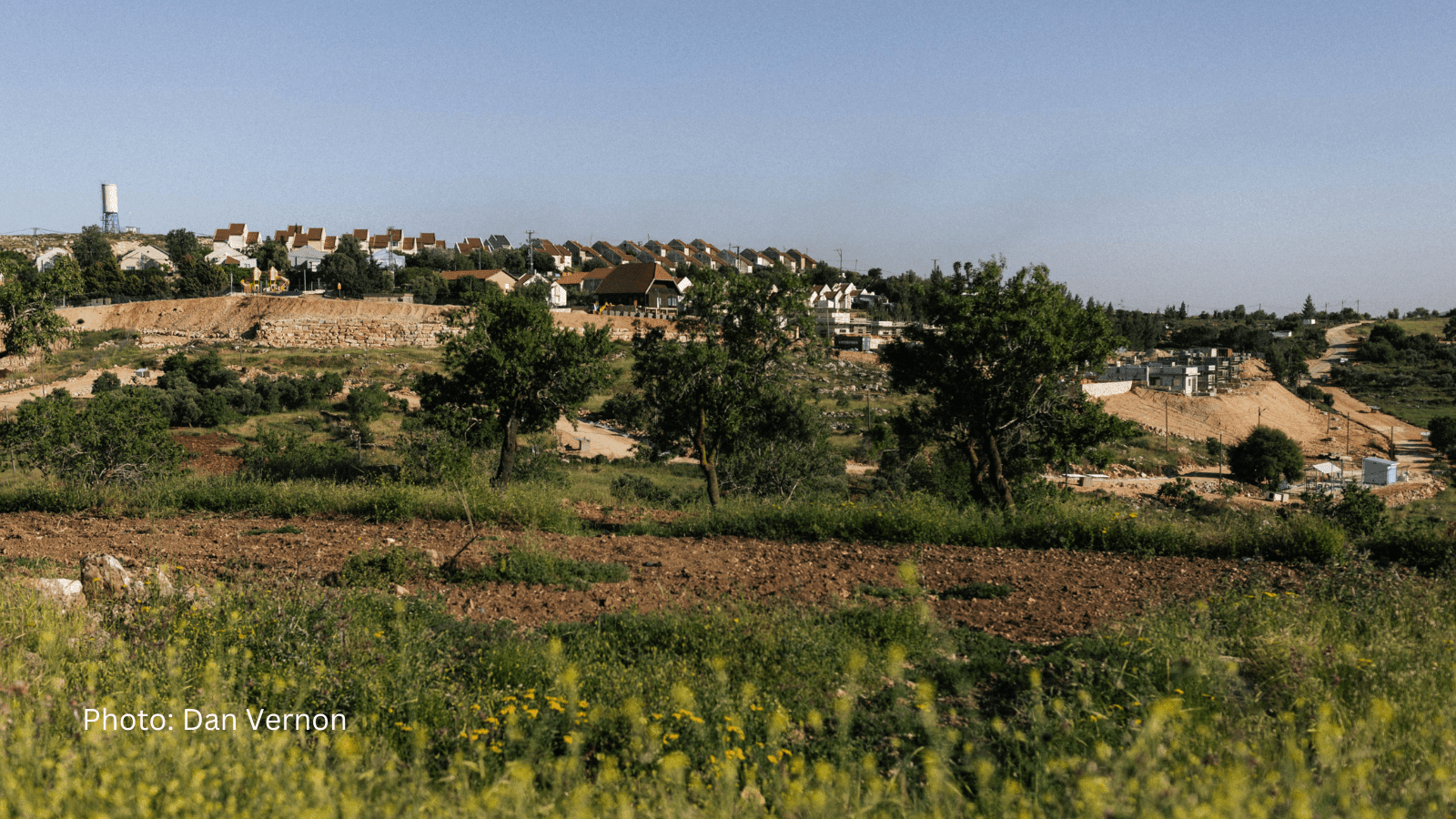

Nonprofit organizations provide significant financial support to the construction, maintenance, and proliferation of Israeli colonial settlements, contributing to and entrenching violations of international humanitarian, human rights, and criminal law in the occupied Palestinian territory (OPT); i.e., the West Bank, including eastern Jerusalem, and the Gaza Strip. Many of these nonprofits function out of the United States (U.S.), Canada, and European States. Commonly under the guise of “charitable purposes,” these nonprofits collect and distribute funds that facilitate international law violations, in contravention of their nonprofit status and the favorable tax designations they receive.

As such, these nonprofit organizations are private entities that effectively function as business enterprises, abuse tax loopholes, and so far have evaded inclusion in the reporting on the United Nations (UN) database of business enterprises involved in Israeli settlement activity in the OPT [hereinafter “UN database”].[1] These nonprofit enterprises operate to maintain the illegal occupation of Palestinian territory by: (i) facilitating the construction and expansion of settlements; (ii) supplying surveillance and military equipment for settlements; and (iii) fuel increasing settler violence, and as such, their activities must come to an immediate end in compliance with the International Court of Justice (ICJ) advisory opinion on the illegality of the occupation.[2]

It is also necessary to highlight the role that involved nonprofit enterprises are playing in the ongoing genocide in Gaza. As calls for the resettlement of Gaza ring through the Israeli government and the public, soldiers are carrying out atrocities to make future settlement rebuilding and the expulsion of Palestinians from the Gaza Strip a reality.[3]

For example, Friends of the IDF (FIDF) is a US-based 501(c)(3) nonprofit headquartered in New York City that financially contributes to projects for the “wellbeing of the soldiers of the Israel Defense Forces (IDF), veterans and family members.”[4] Among the projects that the FIDF undertakes include providing “Lone Soldier Fund Days” and plane tickets for soldiers who volunteer from abroad to join the occupation forces, and to provide “scholarships” to combat soldiers who served in Gaza and the West Bank.[5] According to FIDF, the nonprofit has “transferred tens of millions of dollars in response to IDF requests for support during the Hamas-Israel War.”[6] Thus, FIDF is one example of how nonprofit enterprises are directly providing tens of millions of dollars to the Israeli Occupying Forces (IOF) to support their criminal acts of genocide, war crimes, and crimes against humanity.

The pervasive nature of the nonprofit settlement network extends to the corporate level as well. For example, corporations such as Apple encourage their employees to donate to nonprofits that contribute to the settlement enterprise in the OPT by “price-matching” donations – so they in effect increase or double the original amount donated. Thus, State obligations to protect against human rights abuses committed by third party actors within their territory extends to these corporations contributing to nonprofit settlement activity.

Apple claims to be “deeply committed to respecting internationally recognized human rights in our business operations, as set out in the Universal Declaration of Human Rights, the International Covenant on Civil and Political Rights, and the International Covenant on Economic, Social, and Cultural Rights.”[7] Furthermore, Apple’s “approach is based on the UN Guiding Principles on Business and Human Rights.”[8] However, Apple, along with several other big tech corporations, are flagrantly violating these obligations of international human rights law by directly donating to maintain the illegal occupation of Palestinian territory and contributing to the ongoing genocide in Gaza.

States where corporations such as Apple are subject to jurisdiction are required to protect against human rights abuses committed by these corporations within their territory, including to prevent these companies from encouraging donations to involved nonprofit enterprises.[9]

To this end, Al-Haq urges the Special Rapporteur and third States to:

(i) recognize the pervasive nature of nonprofit enterprise activity in entrenching Israel’s unlawful presence in the OPT, including by financing and maintaining the growth of Israeli colonial settlements in the occupied West Bank, including eastern Jerusalem;

(ii) to hold States accountable for granting tax benefits and allowing these organizations to operate in their jurisdictions; and

(iii) urge their inclusion in the annual update to the UN database.

Please find submission to the Special Rapporteur here.

[1] To receive 501(c)(3) tax-exempt status in the U.S., organizations must satisfy certain requirements, including being “organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes,” complying with restrictions related to lobbying, working within the confines of their mission statement, and ensuring that benefits do not inure to private parties. Moreover, 501(c)(3) organizations may not violate public policy. While §501(c)(3)s generally do not operate for profit, they may undertake certain activities generally associated with for-profit corporations such as earning income from selling goods or services. See 26 U.S.C. § 501, Exemption from tax on corporations, certain trusts, etc., https://www.law.cornell.edu/uscode/text/26/501; Internal Revenue Service, “Exemption Requirements - 501(c)(3) Organizations,” IRS.gov, https://www.irs.gov/charities-non-profits/charitable-organizations/exemption-requirements-501c3-organizations; See also 26 CFR § 1.501(c)(3)-1, Organizations organized and operated for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or for the prevention of cruelty to children or animals; Bob Jones University v. United States, 461 U.S. 574 (1983) (noting that organizations that do not provide “beneficial and stabilizing influences in community life” should not be supported by taxpayers with special tax status).

[2] Legal Consequences Arising from the Policies and Practices of Israel in the Occupied Palestinian Territory, including East Jerusalem, Advisory Opinion, International Court of Justice (19 July 2024).

[3] ‘It is doable’: 10 Likud MKs to attend conference calling for ‘resettling Gaza,’ Times of Israel (16 Oct. 2024), https://www.timesofisrael.com/it-is-doable-10-likud-mks-to-attend-conference-calling-for-resettling-gaza/; [Translated from Hebrew] “A few thousand remain in the north of the Gaza Strip” Israeli Public Broadcasting Corporation (5 Nov. 2024), https://www.kan.org.il/content/kan-news/defense/820691/.

[4] Homepage, Friends of the IDF, https://www.fidf.org/, (last accessed 12 Nov. 2024).

[5] “Stories,” Friends of the IDF, https://www.fidf.org/how-we-help/stories/, (last accessed 12 Nov. 2024).

[6] “About Us,” Friends of the IDF, https://www.fidf.org/about-fidf/, (last accessed 12 Nov. 2024).

[7] Apple, “Our Commitment to Human Rights,” May 2024, https://s2.q4cdn.com/470004039/files/doc_downloads/gov_docs/2024/Apple-Human-Rights-Policy.pdf.

[8] Ibid.

[9] HR/PUB/11/04, Guiding Principles on Business and Human Rights, Art. 1(A)(1), https://www.ohchr.org/sites/default/files/documents/publications/guidingprinciplesbusinesshr_en.pdf.